While generating a reliable, ongoing income in retirement is essential, the amount of that cash flow needs to increase over time due to inflation. Otherwise, you could find yourself losing purchasing power - and depending on your particular situation, it could even come down to cutting back on necessary expenses like food or prescription medications.

Some of your retirement income sources may have built-in “raises,” such as Social Security's cost-of-living adjustments, which are typically implemented every year (although they are not guaranteed).

In other cases, you may have to create an income plan for retirement that accommodates higher payouts over time so that you don't have to reduce your expenses, and in turn, your lifestyle.

Inflation is the rate at which prices for goods and services rise. It can also be translated as a decline in purchasing power. In this case, for instance, over time, the same amount of dollars won't be able to buy the same amount of items or services than they did in the past.

| Year | Price |

|---|---|

| 1970 | $0.25 |

| 1980 | $0.45 |

| 1990 | $0.75 |

| 2000 | $1.00 |

| 2010 | $1.25 |

| 2022 | $1.85 |

Consider how much the price of everyday purchases has risen throughout the years. As an example, in 1970, the price for a cup of coffee was just 25 cents. But by 2022, the same cup of coffee cost $1.85, nearly eight times more.

With that in mind, using just a 3.2% average annual rate of inflation, your income would have to roughly double in 20 years in order to maintain the same lifestyle that you have today. So, for instance, if you are generating $4,000 per month in income now, you would need to bring in $8,000 each month 20 years from now in order to purchase the same (or similar) items and services that you buy today.

It is important to note, though, that just like stock market performance, inflation rates can be averaged out over a period of time. But in each individual year, inflation could be extremely low or significantly high.

Rising prices don't just affect individuals. For instance, the loss of purchasing power that is associated with inflation can impact the cost of living for the common public as well - and this, in turn, could lead to a deceleration in economic growth. In some cases, this might even cause a recession.

What defines a recession is a significant, widespread and prolonged downturn in economic activity. Because recessions often last for at least six months, one rule of thumb for determining whether or not the economy is in a recession is that two consecutive quarters of decline in a country's Gross Domestic Product (GDP) constitute a recession.

There are other criteria to consider when determining whether or not an economic slowdown may be an actual recession. For instance, according to the National Bureau of Economic Research, these factors can include the following:

Recessions usually cause declines in economic output, as well as in consumer demand, and employment - and they often address the economic imbalances that occurred during the preceding economic expansion. This can clear the way for growth to resume after the recession ends.

The most commonly used inflation indexes are the Consumer Price Index (CPI) and the Wholesale Price Index. Typically, an increase in the supply of money is the root cause of inflation.

In addition to higher prices, another way that high inflation can impact your purchasing power in retirement - even if you have a plan in place for increasing your income - is that there is often a lag time between when prices rise and when you start receiving your increased income.

While investors and retirees are typically aware of the issues that high inflation can cause, low inflation can also present some challenges. In this case, low inflation can be a signal of economic problems because it may be associated with weakness in the economy.

As an example, when unemployment is high or consumer confidence is low, individuals and businesses may be less willing to make investments, and consumer spending can slow down. This decline in economic activity can keep prices from being bid up. Inflation tends to decrease when the economy softens. For instance, inflation was low during the Great Recession of 2008-09.

In any case, as you approach retirement, it is essential that you have a plan in place for increasing your incoming cash flow over time. That way, you can better ensure that you don't have to take other measures - such as going back into the working world and/or cutting back on your purchases - as prices continue to go up.

As an employee or a business owner, it may have been possible for you to keep pace with rising prices through the receipt of annual pay raises or increasing the cost of the goods or services your company offered.

But after you retire, keeping your purchasing power up to speed may not be quite as simple. How you go about doing so can depend largely on where you generate your income. Typically, retirees receive income from one or more sources, including:

According to the Social Security Administration, the amount of your average wages that this source replaces can vary, depending on your earnings and when you choose to start these benefits. This pre-retirement income replacement ratio can range from approximately 75% for very low earners, to roughly 40% for medium earners, to about 27% for maximum earners.

| Your birth year | Your full retirement age |

|---|---|

| 1943 - 1954 | 66 |

| 1955 | 66 and 2 months |

| 1956 | 66 and 4 months |

| 1957 | 66 and 6 months |

| 1958 | 66 and 8 months |

| 1959 | 66 and 10 months |

| 1960 and later | 67 |

A formula is used by Social Security to come up with the amount of your retirement benefits. Some of the primary factors that are considered in it include your highest 35 years of earnings and when you opt to start receiving this income.

For instance, you can file for Social Security retirement income as early as age 62. If you do so, however, the dollar amount that you receive will be less than if you waited until your full retirement age (FRA) to file. Your FRA is based on the year you were born. Further, the payment amount will stay lower, even after you have reached your FRA.

Although it is not guaranteed, Social Security recipients will often receive an annual cost-of-living adjustment, or COLA. This is the case, regardless of your age (i.e., before or after your FRA) when you file for benefits. COLAs increase the dollar amount of your Social Security benefit payment, beginning in January of the years they are implemented.

Since 1975, the Social Security general benefit increases have been based on the cost-of-living index, as measured by the Consumer Price Index, or CPI. While COLAs may not be implemented every year, over the past 47 years, the increase has ranged from 0% to 14.3%.

But is this really enough to keep up your purchasing power over time?

Some economists feel that the CPI may not be the best measure of inflation when it comes to determining the Social Security cost-of-living adjustment. The CPI measures inflation as experienced by consumers in their day-to-day living expenses. However, according to the U.S. Bureau of Labor Statistics, the “best” measure of inflation can depend on the intended use of the data.

All Social Security retirement income benefit recipients are eligible for cost-of-living increases (as well as the recipients of Supplemental Security Income, or SSI). So, there is no need to individually apply for this income adjustment.

| Year | COLA | Year | COLA | Year | COLA | Year | COLA |

|---|---|---|---|---|---|---|---|

| 1975 | 8.0 | 1987 | 4.2 | 1999 | 2.5 | 2011 | 3.6 |

| 1976 | 6.4 | 1988 | 4.0 | 2000 | 3.5 | 2012 | 1.7 |

| 1977 | 5.9 | 1989 | 4.7 | 2001 | 2.6 | 2013 | 1.5 |

| 1978 | 6.5 | 1990 | 5.4 | 2002 | 1.4 | 2014 | 1.7 |

| 1979 | 9.9 | 1991 | 3.7 | 2003 | 2.1 | 2015 | 0.0 |

| 1980 | 14.3 | 1992 | 3.0 | 2004 | 2.7 | 2016 | 0.3 |

| 1981 | 11.2 | 1993 | 2.6 | 2005 | 4.1 | 2017 | 2.0 |

| 1982 | 7.4 | 1994 | 2.8 | 2006 | 3.3 | 2018 | 2.8 |

| 1983 | 3.5 | 1995 | 2.6 | 2007 | 2.3 | 2019 | 1.6 |

| 1984 | 3.5 | 1996 | 2.9 | 2008 | 5.8 | 2020 | 1.3 |

| 1985 | 3.1 | 1997 | 2.1 | 2009 | 0.0 | 2021 | 5.9 |

| 1986 | 1.3 | 1998 | 1.3 | 2010 | 0.0 | 2022 | 8.7 |

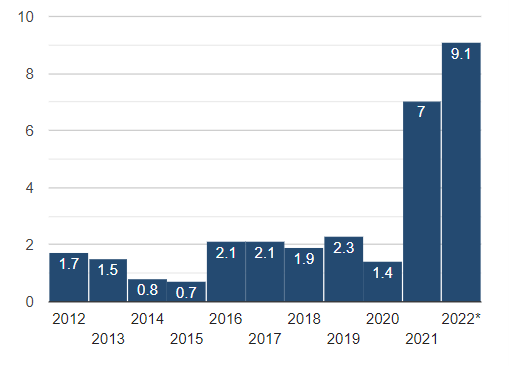

In October 2021, the Social Security Administration announced a 5.9% COLA for Social Security recipients in 2022. Going forward into 2023, it is estimated that Social Security recipients will receive a cost-of-living adjustment of 10.5%.

The Social Security COLA for 2023 is expected to be substantial compared to previous years. Even so, it might not be as big of a deal as some people think. For instance, the Social Security COLA 2023 estimate is 10.5%, but with inflation at over 9% - versus just 1.4% in 2020 - the actual rise in income isn't very much.

So, even with higher monthly Social Security checks, retirees may still not be able to maintain a comfortable lifestyle - particularly if other expenses, such as health care and long-term care services - are added into their outgoing budget.

Although most companies no longer offer defined benefit pension plans, there are some retirees who receive income from this source. Unlike Social Security payments, most pensions do not offer a cost-of-living adjustment that keeps pace with the current inflation rate.

While there are some pensions that will periodically increase recipients' payments via cost-of-living adjustments, those raises are oftentimes small relative to the actual rate of inflation in the economy.

For instance, based on figures from the U.S. Department of Labor, the Consumer Price Index jumped 8.5% in March 2022 from a year prior, which is the fastest 12-month increase since December 1981. This means that a “basket” of items that cost $100 one year ago would now cost $108.50, on average.

Some of the biggest contributors to this included food, housing and gasoline - categories that have a significant impact on the typical American. In fact, housing, transportation and food accounted for nearly two-thirds of the average household budget in 2020.

With that in mind, the real value of pensions can often go down. For example, an inflation rate of 1% would reduce the value of a $25,000 annual pension benefit to just $20,488 after 20 years. A 2% inflation rate would erode its original value by one-third, to roughly $16,690.

So, those who are counting on raises in their pension income will likely have to develop a strategic plan for increasing their cash flow in other ways if they want to keep their purchasing power up.

Many retirees also rely on cash flow that is generated from personal savings and investments. Typically, though, there is a tradeoff between risk and reward. In other words, higher risk equities could offer the opportunity for growth that may outpace inflation. But, given the volatile stock market of late, they can also increase the risk of loss - and this can be detrimental for retirees.

Conversely, safe investments that pay out a preset interest rate - regardless of what happens in the stock market - usually pay pitifully low returns that often do not even meet, much less beat, inflation.

There are some strategies for safely increasing retirement income over time. One is to develop a plan for using your fixed, guaranteed Social Security income alongside an investment plan that includes stocks and bonds for supplementing cash flow.

Another is to consider purchasing a fixed indexed annuity that includes an increasing income rider. With many of today's annuities, the income riders offer a guaranteed amount of income for life.

But, the dollar amount of each payment stays the same. Therefore, if you live for 20 or more years in retirement, your income will likely shrink over time as compared to the prices of the goods and services that you need to purchase.

As an alternative, fixed index annuities that feature the ability to increase income will oftentimes provide for increases that are based on an underlying index or the performance of the Consumer Price Index (CPI).

These types of annuities track one or more underlying market indexes, such as the S&P 500. If the index performs well during a given time period - such as a contract year - then the annuity is credited with a positive return, usually up to a maximum percentage. However, if the underlying index performs poorly, there is no loss incurred in the annuity's account value.

So, for instance, if the index - subject to various upside limitations like caps, spreads and participation rates - increases by 4% during its distribution (or income payout) phase, then the lifetime income payment that is generated by the annuity's income rider would also go up by 4%.

While your Social Security payments are likely to rise in 2023, expenses related to housing, food, health care and other essentials are also likely to go up. So, each of these could end up cancelling each other out.

The good news is that there are still ways to increase your retirement income over time so that it helps keep pace with inflation - regardless of how long you (and your spouse, if applicable) live and require the cash flow.

Using annuities to supplement your retirement income add a degree of certainty that can allow you to focus on other matters - such as spending time with loved ones or relaxing on the beach - knowing that you will receive regular “pay raises” in the future.

If you opt to use an annuity as part of your retirement income strategy, though, it is essential that you first seek the advice of an experienced financial professional. While annuities can offer many nice features, they also come with a myriad of “moving parts.” So, an expert can assist you with narrowing down the right annuity for you.

Alliance America is an insurance and financial services company dedicated to the art of personal financial planning. Our financial professionals can assist you in maximizing your retirement resources and achieving your future goals. We have access to an array of products and services, all focused on helping you enjoy the retirement lifestyle you want and deserve. You can request a no-cost, no-obligation consultation by calling (833) 219-6884 today.