Millions of Americans rely on financial advisors, brokers and other financial professionals to help them plan for retirement. It’s assumed that as they age, these professionals will shift their assets to more conservative investments. This strategy often includes annuities, which can be wonderful tools for creating income in retirement. Be wary, though, of variable annuities. These annuities come with some major risks and fees. We’ll discuss the risks and a better solution.

Before we dive into the details on variable annuities, let’s briefly review the concept of asset allocation. Asset allocation can be thought of as the purposeful selection of investments taking risk, need and goals into account. The result of asset allocation is the division of a nest egg or portfolio into differing kinds of assets. Common assets, from most to least risky include:

As you age, a general rule of thumb is to reduce your exposure to the higher-risk asset classes, like stocks, and increase percentage of lower-risk assets like bonds and bond funds. A common strategy for asset allocation is the “100 minus your age” rule. This rule states that the percent of your portfolio exposed to the stock market should equal 100 minus your age. So, if you’re 55 years old, you should have no more than 45% of your portfolio in stocks.

This is important because the stock market can be risky, and losing large parts of your wealth close to retirement age can put a serious dent in your financial security. Consider that since 2000, there have been three major bear market crashes: 2000-2002, 2008-2009 and 2020. The average decline during these bear markets was 43%.

Losses of this magnitude can ruin retirement plans, so it’s crucial to use asset allocation to reduce your risk of loss. A common tool used near and in retirement is an annuity. Annuities are considered very safe, as they are usually guaranteed. Traditional annuities are guaranteed in two ways:

One downside to traditional annuities is that they tend to pay a low interest rate, making it difficult to accumulate large nest eggs without making large contributions.

To combat this shortcoming, the variable annuity was created.

A variable annuity is an annuity whose value is dependent on the investment performance of an underlying portfolio of securities or mutual funds. In theory, this feature allows for greater earnings and larger accumulated values. If realized, this would allow for larger income streams.

There are two big concerns with variable annuities, though:

We already reviewed the necessity to avoid large losses in or near retirement, so you can see how owning an annuity that isn’t guaranteed might not be a great idea.

The other risk factor with variable annuities is the cost. For one thing, variable annuities often come with higher or longer surrender charges. These surrender charges are a way of recouping the commission the insurance company paid to the selling agent or broker.

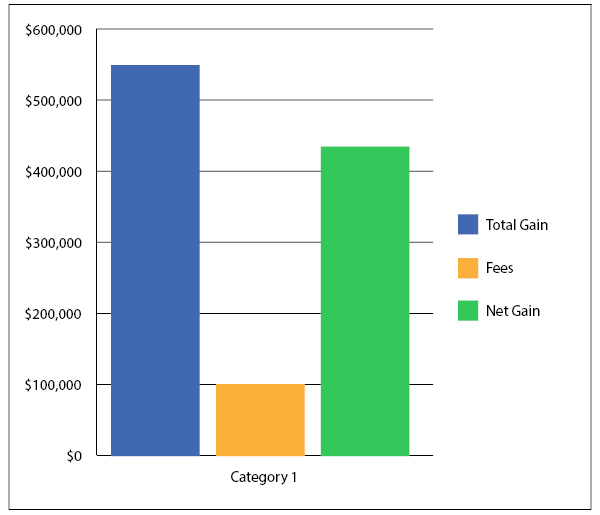

Besides surrender charges, you can be charged investment management fees, which can vary from 0.25% to 2%. Mortality expenses and administrative fees can push the total fee cost to 3% or more on some variable annuities. Fees of 3% are considered very large and can lower your investment returns in a big way. According a web-based fee calculator, if you had $250,000 invested in a variable annuity, and you earned 8% returns, you’d lose out on over $100,000 in gains over the course of 10 years.

Figure 1 Impact of 3% Fees on $250,000 Nest Egg

If you like the idea of guaranteed income, and protection from losses that come from traditional annuities, but still want the ability to earn higher interest, consider indexed annuities.

An indexed annuity is a fixed annuity, like a traditional annuity, but with the ability to earn market-based returns. The best part is that, unlike variable annuities, you are protected from losses.

An indexed annuity can be thought of as offering two accounts:

You can allocate your existing accumulated cash value, as well as ongoing premiums, to either or both accounts. You can allocate your cash values in any ratio you desire. And, you can also make changes to your choices on an ongoing basis.

The rate earned on the indexed account is based on the performance of your chosen indexes. Indexes are usually tied to major asset classes like:

The way your indexed interest rate is calculated can vary by insurance company, but is generally dependent on these values:

The index performance can be calculated in several ways, including one year point-to-point, or multi-year performance. You’ll be able to choose your method.

The participation rate is the percentage of the index performance that can be attributed to your accumulated values. Common participation rates range from 80% to 100%.

The rate cap is the maximum interest rate that will be credited to your account, regardless of index performance. Rate caps can vary widely, from 4% to uncapped annuities. It’s important to keep in mind that the participation rate is applied first, and then the rate cap.

As an example, assume that your chosen indexes returned 15% during the year, that the participation rate is 90%, and the rate cap is 7%. In this case, the return (15%) is multiplied by 90%, which gives 13.5%. This amount is higher than the rate cap, so your interest rate would be 7% for the year.

Let’s say that the stock market crashes and enters a bear market. Your indexes are down 22%. With a variable annuity, you would experience an actual loss of cash value. But, with an indexed annuity, you would earn an interest rate of 0%. You’re totally safe from losses. And, if you have part of your cash value in the fixed account, you’d make a small gain.

This is the beauty of the indexed annuity: the potential for higher interest rates than traditional annuities, but with none of the downside risks of variable annuities. They are a much better option for your retirement nest egg.

Though indexed annuities have much lower fees than variable annuities, they still do have fees and charges, especially surrender charges. For this reason, they should only be chosen as part of your overall retirement plan, and you should commit to the strategy for the long term, at least 10 years. Make sure to work with a qualified financial professional to select the indexed annuity that will best accomplish your goals. You’ll also want to work with a financial professional to select and monitor your indexing strategy over time.

Alliance America is an insurance and financial services company. Our financial professionals can assist you in maximizing your retirement resources and achieving your future goals. We have access to an array of products and services, all focused on helping you enjoy the retirement lifestyle you want and deserve. You can request a no-cost, no-obligation consultation by calling (833) 219-6884 today.